The question of how to keep private-sector rents in check has become ever more relevant of late. In France, following the example of organizations such as the Abbé Pierre Foundation, proposals to limit rent increases when a tenancy ends—and not just during the lease period—have brought this issue back to the fore. The arguments in favor of interventions of this kind are broadly linked to two key trends observed in recent years: first, the proportion of household income spent of housing has been increasing; and second, landlords have been taking advantage of changes of tenancy to impose very steep rent hikes. [1]

Consensus on the adverse effects of rent control

This renewed interest is, however, also likely to arouse criticism of the unintended adverse consequences of rent regulation, and more specifically the precedent of interwar rent control in France and the French rent-control law of 1948. Such criticism is firmly entrenched, not just among landlords’ associations (which is hardly surprising) but also within the academic world. As soon as rent control was introduced in the interwar period, it garnered an extremely negative reputation for itself and its effects on real-estate investment [2]: supposedly, by reducing the profitability of these investments, rent control had negative consequences on new construction, rental investment and building maintenance. The concomitance, during the interwar period and following the 1948 law, of rent control, a slow deterioration of old housing stock, and a long-term housing shortage gave credence to this view, even though it was based on only a small amount of research and empirical data—and even though these problems did not occur immediately after the First World War.

The aim here is not to attempt to justify the special regime of the interwar period, nor the 1948 law, which are each based on specific and questionable mechanisms (see Inset 1), but rather—with the aid of more precise data from recent research—to call into question the quasi-consensus [3] on the equation linking rent control, investment profitability and property investment. More specifically, by using the results of a long-term study that monitored the portfolio of a property-management firm in Lyon, east-central France, between 1860 and 1968 (see Inset 2), we found that the arguments put forward to explain the adverse effects typically attributed to rent control are in fact quite debatable. That said, we do not seek to enter into detailed discussion of the effects of rent control on new construction and renovation here, which would require long explanations that go far beyond the scope of this article; instead, we shall focus on one key factor, namely the profitability of real-estate investment, and how it is affected by periods of rent control.

Inset 1: rent-control mechanisms

In France, the 20th century was marked by a long period of rent regulation. This period began in 1914 with a moratorium on rents for households where one or more members were mobilized in the war effort (gradually extended to other categories of tenants). The special rent regime that followed after the First World War was not the result of clearly adopted guidelines or policies. Rather, it consisted of a raft of separate measures (36 decrees and laws passed between 1919 and 1936), presented as provisional and sometimes mutually contradictory, implemented in response to a situation continually perceived as exceptional. Rents were limited by applying a coefficient to 1914 rents (for example, in 1926, rents could not exceed twice their 1914 rates). The coefficients were determined according to the category of apartment (the lowest rents were those primarily concerned by this measure) and were continuously revised and extended to other premises. From the early 1930s onward, caps were also imposed on rent increases following a change of tenancy.

The 1948 law sought to bring this special regime to an orderly end; however, it was also very complex, insofar as it introduced different categories of apartments and required the calculation of “adjusted floor space.” Depending on different authors’ viewpoints, it has been portrayed either as a new legislative straitjacket or as a means of returning to free-market conditions. It was, in fact, both: as soon as an eligible dwelling was rented out to new tenants, it was no longer deemed to be within the scope of this law; however, in cases where there was no change of tenancy, eligible dwellings remained under this regime for a period of time that was in some cases very long. In the early 1950s, rents regulated by the 1948 law were increased significantly, but the gap between free rents and controlled rents rapidly grew again. It was this gap between the two that would be cited as the main cause of the law’s negative effects.

Low rental yields at the heart of criticisms

In the early 1920s, in the face of rent-control measures, landlords were mainly outraged by infringements of property rights but, quickly, more economic assessments appeared. They mainly consisted of pointing out the gap between the increases authorized by legislation and the rise in prices in general, which affected management costs in particular. [4] In her virulent criticism of the special rental regime, Marie-Madeleine Pitance [5] saw it as one of the main factors contributing to the sluggish rate of housing construction and the under-maintenance of housing. Without forgetting, of course, the role of rising interest rates and construction costs, as well as the “unfair competition” that the first programs of social housing (habitations à bon marché, or HBMs) represented for traditional contractors, this criticism blames rent control for the low profitability of newly built dwellings, even though rent control did not apply to new housing. Rent regulation is therefore presented as the key factor behind the changing housing context during the economic upheavals of the interwar period, whereas it was in reality only one factor among others, not least a severe shortage of working-class housing dating back to the 19th century. [6]

The arguments put forward by landlords’ associations had been made known from the beginning of the interwar period onward. But it was above all after the Second World War, and in particular following the publication of (relatively lenient) research by economist Françoise Carrière in 1957, [7] that the critical approach to rent control in the academic world was structured. The focus of this approach was the drop in returns on investment in real estate. Carrière’s work was often built upon by subsequent research, but without the provision of any additional data to support the central element, namely rental yields (i.e. the rent-to-price ratio) [8]: Carrière estimated that, while gross yields did not collapse after the First World War, net yields (i.e. taking account of costs) fell dramatically. The increase in management and maintenance costs compared to rents is believed to be the cause of underinvestment in buildings. Carrière’s book is characteristic of research on the subject: its method is based on comparisons of series (e.g. prices and rents) and not on direct measurement of returns. The difference between the two is significant: in the first case, which is more approximate, the average rent is compared with the average price, while in the second case the average is calculated of all rent-to-price ratios—the two calculations are quite different. [9] The second solution, however, requires sources that are difficult to access. In the Carrière book, for example, the gross yields cited come from data supplied by experts, and no data on net yields are provided. [10]

Inset 2: methodology and the long-term monitoring of a sample of buildings [11]

The results presented here come from research funded by the ANR (French National Research Agency), which is based on a review of the accounting records for the buildings managed by of a private property-administration firm in Lyon, founded in the 1860s and still in operation today, which granted access to its archives. A total of 64 buildings managed for more than 50 years (with conventional leases) were selected, with a focus on the period from 1890 to 1968. The sample chosen is sufficiently diversified to offer an acceptable representation of Lyon’s central neighborhoods, although this means a lot of them are apartment buildings intended for the middle or upper classes. The phenomena relating to profitability mentioned here are even more obvious for very run-down working-class buildings (lodging houses, slums), which exhibit very high profitability rates and endemic under-maintenance. The registers provide information on rents per apartment (as well as their characteristics: floor, surface area, number of rooms), sums collected by landlords and charges (including tax charges such as property taxes). These data were supplemented by the reconstruction of the ownership histories of the buildings, essentially based on the transcriptions of the deeds of sale kept at the mortgages. This source makes it possible to process the recent period, which is not possible due to the time required to consult the notarial archives. In addition to the succession of owners, it was possible to find all the sale prices for these buildings and calculate the profitability ratios.

High yields maintained, despite rent control…

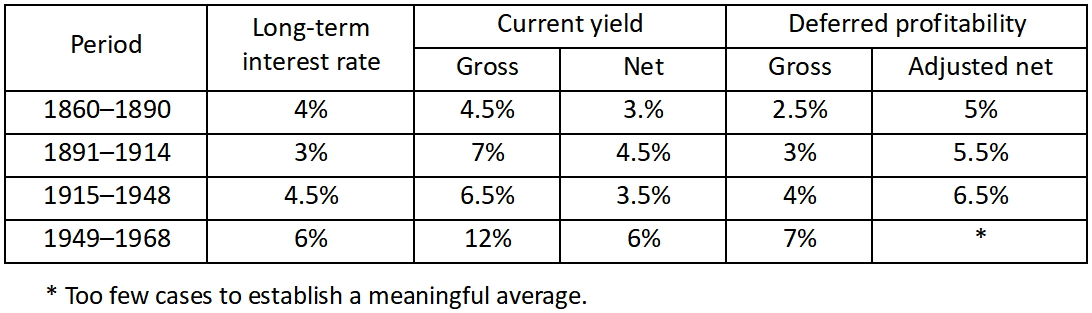

However, the results of our survey do not confirm this theory of falling real-estate returns. On the contrary, net returns remained high, as building prices adjusted to rents. To support this analysis, we rely on the measures of gross and net returns that have been possible to achieve. But this is only the first step. Indeed, the returns observed at the time of sale can be misleading for several reasons: an increase in rents improves it, major repairs deteriorate it, as well as a relative increase in the price at the time of sale compared to the rent. The historical perspective makes it possible to measure ex‑post profitability retrospectively, that is to say by taking into account all the income received by the owner over the period in which he owns the building (we shall call it “deferred profitability”). This was done in two ways: first, without taking into account the resale price (net deferred profitability), and second, by including it in the calculation (net deferred profitability plus). [12]

Interpretation: in sales completed between 1860 and 1890, buyers would have earned an average yield of 4% if they had invested the amount in annuities. On average, they obtain a gross instantaneous yield (total rental income/price) of 4.5%, net of 3% if charges and transfer taxes are taken into account.

These results show first of all that the net yields between the wars were not as low as might have been expected, even at levels comparable to those at the beginning of the Third Republic. While the gap between net and gross returns is widening (and even more so after 1948), the main difference with the previous period is that interest rates exceed the level of real-estate returns.

… and profitability rates higher than interest rates

The observation of deferred returns completes this picture. First, it shows that buildings purchased during the Belle Époque were particularly affected by the special rental regime and inflation. But it also shows that interwar buyers on average achieved better profitability than they might have expected. While this is partly due to the fact that they are resold after 1948, a significant part of their management period takes place during the special rent regime. The contribution of this measure of profitability is twofold. At first, it confirms the fairly good resistance of real-estate investment over a long period, contrary to the generally widespread idea of a collapse of the stone following rent control. This is all the more true since we take into account the resale value.

The after-the-fact measurement of profitability also shows that the net instantaneous yield (and a fortiori the gross yield) can be quite misleading. Certainly, certain events such as the 1914 moratorium, rent legislation or interwar inflation cannot be anticipated, but some of them are, at least in part, foreseeable. The appreciation of rents, particularly if increases during the lease term are indexed, is an example. The real profitability measured a posteriori is frequently higher than expected by the net instantaneous yield at time t, which means that the profitability of real estate is also frequently underestimated. This is an interesting argument to put forward in a context where support and incentives for rental investment are subject to a number of criticisms regarding their cost and targeting.

Should rents be controlled?

The remarks developed here lead us to put into perspective the impact of rent control on under-investment in real estate. Certainly, they concern specific historical contexts whose characteristics are not present at the present time. The effects of rent control can only be understood in relation to a range of factors that characterize housing markets in successive periods. Moreover, the previous arrangements are open to criticism: the chaotic nature of the special rent regime in the interwar period cannot serve as a model any more than the 1948 law and the creation, in fact, of a dual market, one regulated and the other “free.”

Nevertheless, the assumption that profitability will collapse as a result of rent control is incorrect. The proposal to limit rent increases upon change of tenancy does not therefore seem likely to cause a significant drop in the returns on real-estate investment either. It also avoids the pitfall of the 1948 law (which characterizes the current situation, albeit in a less extreme manner) by bringing rent increases upon change of tenancy and during the lease period closer together. Even beyond this proposal, it is advisable not to confine oneself to a reductive vision of real-estate investment, focused solely on the rent–price ratio—a vision that can alter the effect of public policies aimed at influencing rental investment.