“We don’t take tenants under 622”: the response from Ganief, a real-estate agent in Cape Town, is swift. [1] In order to obtain a lease in International Housing Solutions’ housing portfolio, a credit score above 622 is required. From his tablet, this agent would simply need to enter the applicant’s ID number on the credit bureau platforms to instantly obtain the corresponding credit score. In contrast to the stereotypes associated with townships [2] and informality, the housing market in South Africa is highly digitized, as evidenced by the daily use of credit scoring by real-estate agents.

As a result, the city of Cape Town can be considered a laboratory for analyzing two processes observed in metropolises in the Global South and the Global North alike: the reconfiguration of the real-estate market by digital technologies, accelerating the transformation of housing into a financial asset; and the consequent renewal of urban segregation in the age of platform capitalism.

Digital identifiers to rebuild South Africa’s real-estate market

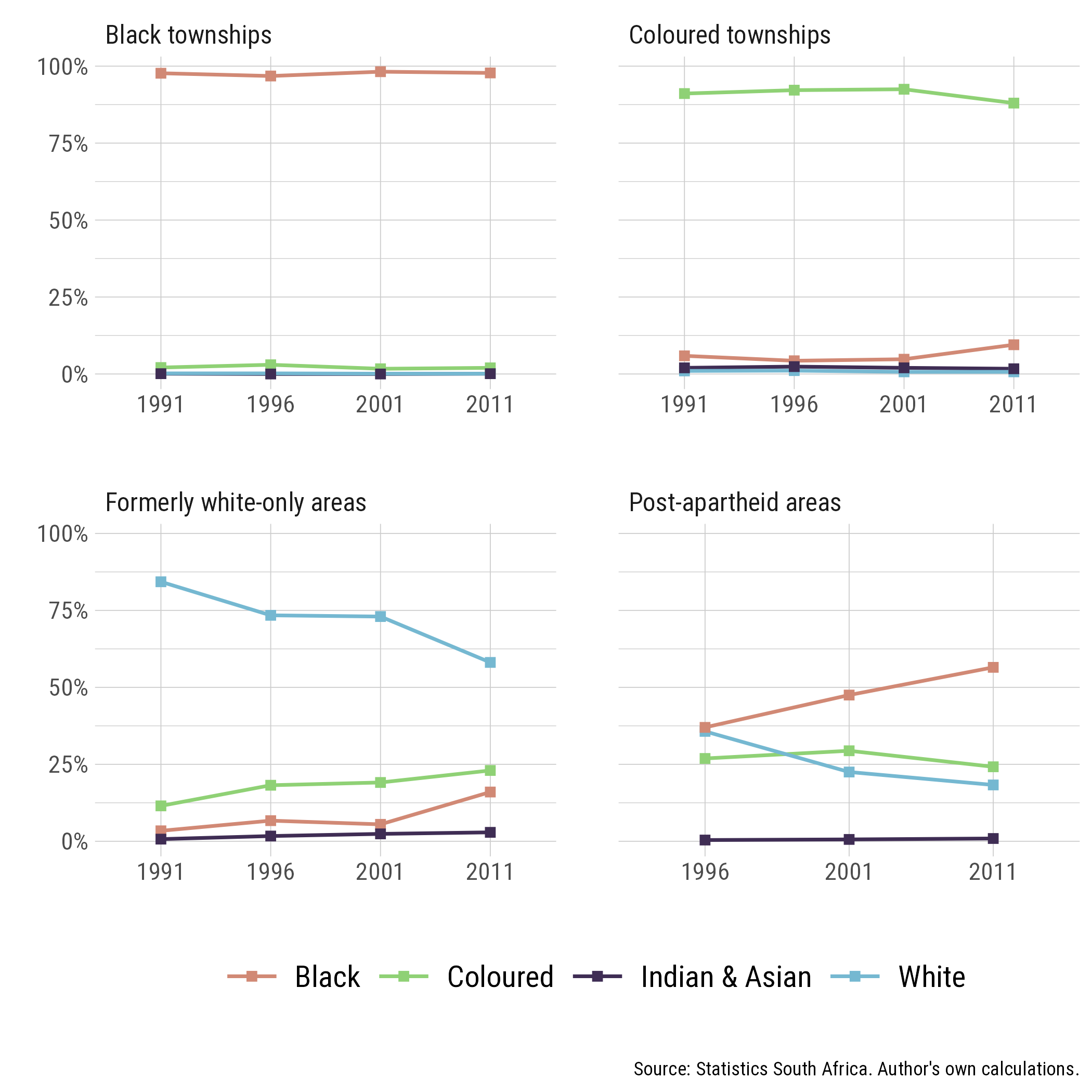

In South Africa, the market was shaped by colonialism and apartheid, the legal mechanisms of which enabled the dispossession of people of color from land to the benefit of the white demographic minority, while prohibiting the free sale of real estate between people of different racial categories, resulting in extreme levels of urban segregation and inequality (Western 1981). In fact, apartheid was structured around a racist regulation of the market which, through the invention of racial categories, imposed homogeneity between the inhabitant and his or her neighborhood. Until 1986, the black majority of the population was denied access to private property in urban areas, and the “Coloured” [3] population was only eligible for mortgages in the specific Coloured townships where they were segregated. Today, every South African is free to live wherever he or she chooses, according to his or her financial capabilities, but Cape Town remains highly segregated (Figure 1). And yet, the market has evolved: today, all it takes is one click on a property portal to find out about price trends, apply for a loan or see the presence of major South African agencies in the townships as well as in the former whites-only districts.

Interpretation: in 2011, Coloured people represented almost 25% of the population of formerly whites-only neighborhoods.

Author: Julien Migozzi, 2020. Source: Statistics South Africa.

Digital technologies have played a key role in this reconfiguration of the market, which is now defined as a continuous flow of data, the collection and analysis of which not only organizes the sale and rental of property, but also classifies homes, individuals and neighborhoods according to risk and profit metrics. This flow is structured around two identifiers: the identity number, assigned to each South African citizen, and the cadastral number, assigned to each dwelling. Digitized, these identifiers enable tasks to be automated, such as the valuation of a property or the consultation of a credit score—that is, an individual rating measuring the creditworthiness of a credit applicant. Public institutions have played a key role in this process. A master in the art of classifying its population, the South African state is proving to be a pioneer of biometric technologies for governance and surveillance purposes (Breckenridge 2014): from 2011, the Smart ID Card program distributed a digital identity card to every citizen. At the same time, metropolises such as Cape Town are at the cutting edge of geographic information systems, notably to automate the calculation of property taxes.

Market players have thus deployed an “informational dragnet” (Fourcade and Healy 2017) orchestrated by real-estate platforms (Shaw 2018). On the one hand, real-estate portals organize the encounter between agents and households. On the other, banks, agencies, brokers or developers connect to credit bureaus, which model and assess individuals’ financial histories, as well as to data analytics companies that market housing data (sales history, surface area, nearby amenities, etc.). Absorbing data from major retailers (supermarkets, clothing stores, home furnishings or electronic equipment, etc.), banks and public institutions, credit bureaus are able to rate, in an automated fashion, virtually the entire South African population. The rating generally ranges from 0 to 999, and takes into account payment history, outstanding balance, age and type of credit held. This informational dragnet, historically woven by the public authorities, was fleshed out by the explosion in consumer credit in the 2000s. By aggressively marketing their credit cards, major retailers have contributed as much to the population’s indebtedness as to the expansion of consumer databases. The adoption of credit scoring thus reconfigured the real-estate market, placing data at the heart of the system.

Financialization, bit by bit

Credit scoring plays a central role: against a backdrop of economic stagnation, banks have systematized credit scoring since 2007 in order to select loan applications, thus renewing socially and racially exclusive banking practices. Indeed, the sharp rise in property values over the decade 2000 and stagnating wages have reinforced the need for a large part of the population to have recourse to the loan, which remains accessible only to the top quintile of the population in terms of income. Above all, it’s not enough to have a regular income: you also need to demonstrate a flawless consumption history in the eyes of the algorithms. As one Cape Town real-estate agent put it, “Banks: they want your DNA.” Yet, in a landscape of massive and racialized indebtedness (James 2014), home loans thus regulated by scoring remains an extremely selective financial product. At a small real-estate agency in Khayelitsha, Cape Town’s largest black township, the rejection rate is close to 70% of applications.

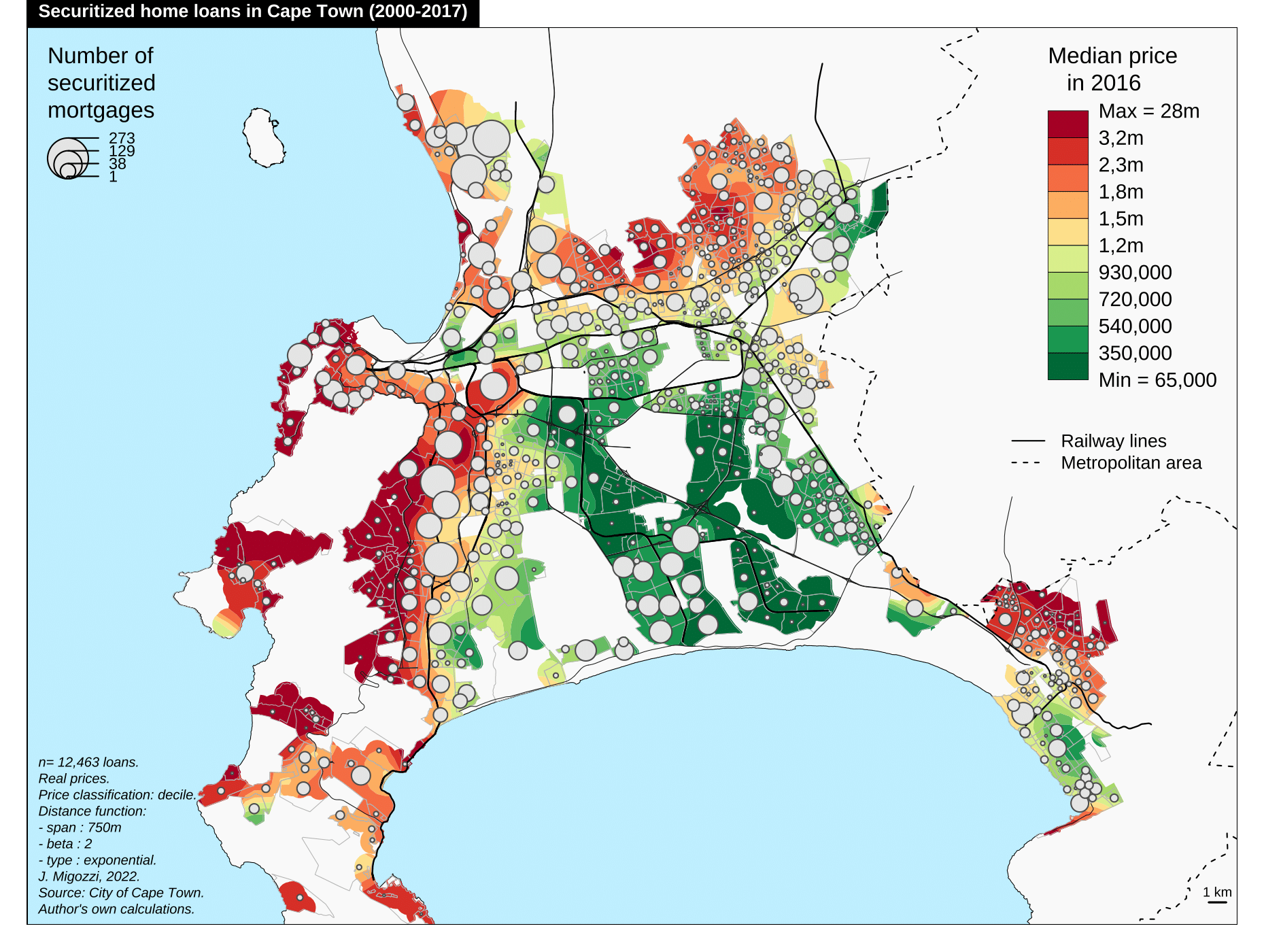

For the remaining 30%, however, digital technologies have led to the reconstruction of a previously dislocated market, by incorporating socially and “racially” very different populations and neighborhoods into the same informational dragnet. The abundance of data on housing and individuals forms the basis of a digital architecture which, when mobilized by real-estate professionals, enables a financialization of housing “bit by bit,” in both the acquisition and rental markets (Migozzi 2020). South African banks have embraced the practice of loan securitization, which consists of reselling their mortgages in the form of financial securities on international markets, thanks to the acute selection made possible by data. However, this financialization is based on an opposite class structure to that which produced the subprime crisis. In Cape Town, it does not target the underprivileged population of color, but the owners of neighborhoods formerly reserved for whites, as well as the salaried middle class of the townships, notably from the civil service (Figure 2). At the same time, listed real-estate investment trusts (REITS) and investment funds invested in the rental segment by purchasing apartment lots, extending their activity to residential property previously considered too risky and unprofitable. But inflation changed all that, triggering a surge in rental demand. Above all, the emergence of these institutional investors is explained by the technical possibility of using credit scoring to sort out applications and thus eliminate the “bad tenant,” in order to minimize the risk of non-payment and thus the vacancy rate.

Author: Julien Migozzi, 2020. Source: Statistics South Africa; Deeds Office.

What is more, in addition to the housing policies that have enabled 4 million poor households to become homeowners, the South African government has been supporting this financialization since 2012 with the Finance-Linked Individual Subsidy Program, which grants financial assistance to first-time buyers with modest salaries—but only if and after they have obtained a loan, and thus passed the scoring filter. In this case, access to public assistance is conditional on the practices and decisions of the banking sector.

Urban segregation in Cape Town: digitized filtering and the reproduction of inequalities

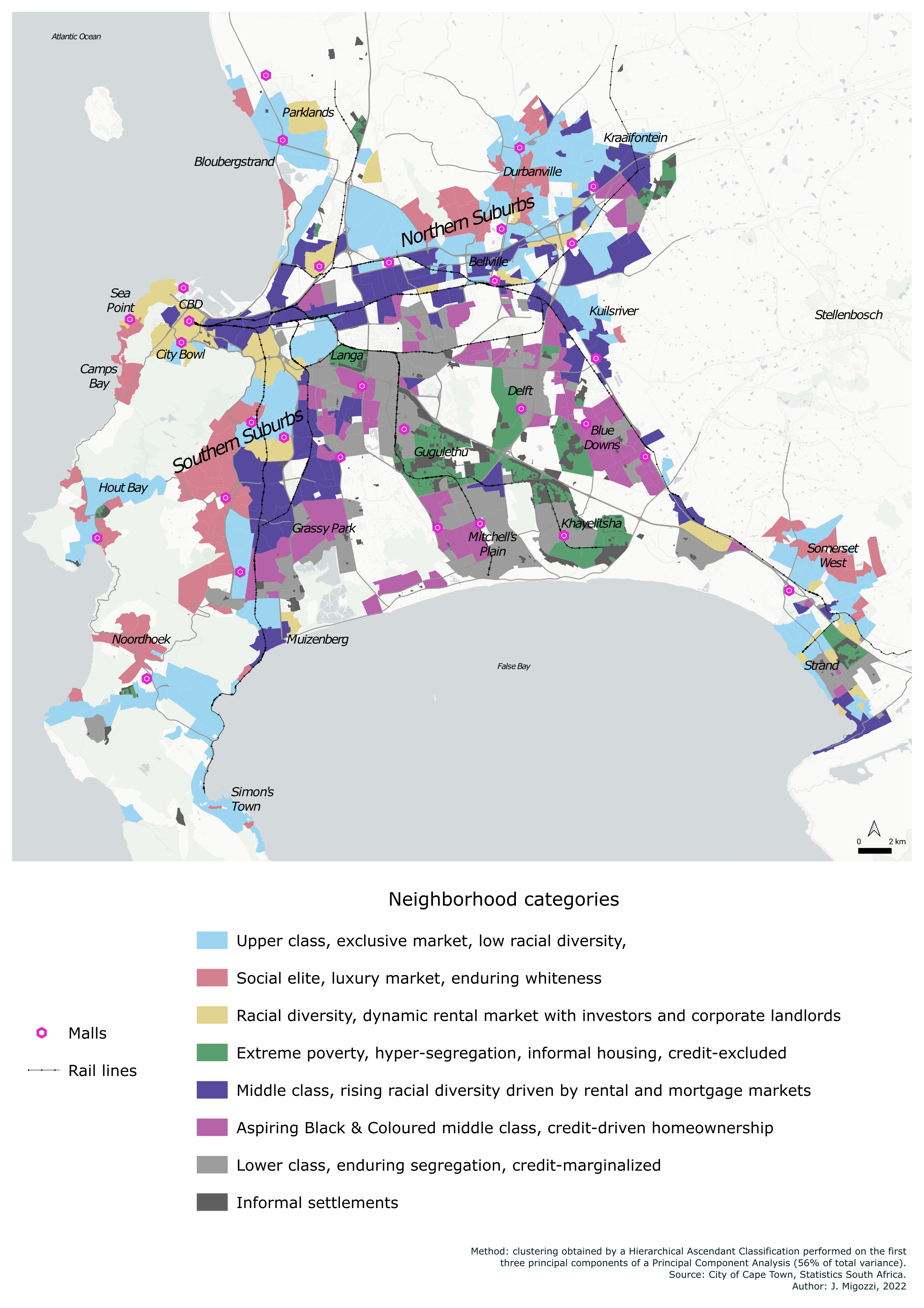

In Cape Town, this digitization and financialization of the market, structured around credit scoring, is renewing forms of urban segregation in two ways. On the one hand, it tends to reduce racial segregation in new housing developments sold by the private sector, where segregation based on income and a transformation of urban forms are developing. Apartments are becoming increasingly popular as a real-estate product. Developers are reproducing the same model on the outskirts of Cape Town, Johannesburg and Durban: a secure residential complex of three- to four-storey buildings built around an inner courtyard. The market is thus producing an unprecedented verticalization and densification of the urban front (Figure 3), which was historically dominated by the single-family home model. This is where the new middle class, filtered through the market, is concentrated, forming the crucible of a new South Africa. Intermediate rents and prices attract white, black and Coloured populations whose social trajectory and residential mobility share a common thread: their passage through two filtering mechanisms, that of affordability, produced by the relationship between price and income, then that of scoring, in order to gain access to leases or loans, and to potentially build up housing wealth through property ownership. These neighborhoods are thus spaces where racial diversity contrasts with the rest of the city. They also bear witness to the fact that class, rather than race, structures the new processes of residential segregation in metropolitan South Africa (Seekings and Nattrass 2005), as evidenced by the contemporary heterogeneity of the urban fabric (Figure 4).

© Julien Migozzi, 2017.

Typology obtained by hierarchical agglomerative clustering (HAC) performed on the first three principal components of a PCA (56% of total variance). The method and neighborhood profiles are detailed in Chapter 9 of the author’s dissertation, available online.

Author: Julien Migozzi, 2020. Source: Statistics South Africa; Deeds Office.

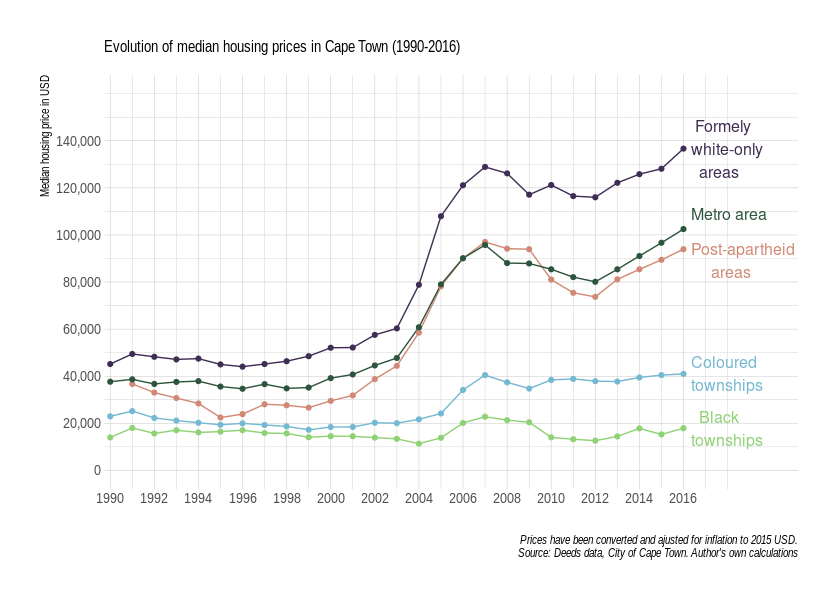

But this urban change remains limited to certain areas: at a metropolitan level, two factors explain the maintenance of extreme racial segregation. The adoption of digital technology has left intact the urban inequalities forged by colonialism and apartheid, particularly in terms of price geography and wealth distribution. First, while townships have integrated real-estate platforms, property values there remain systematically lower than in the rest of the conurbation (Figure 5). In fact, the gap with formerly whites-only areas has widened. Second, banks will not grant 100% mortgages above 1.5 million rand, which means that the buyer’s own assets and savings, which are much lower among black and Coloured populations, are mobilized. As a result, the uneven rise in property values and the construction of mortgages, by reinforcing inequalities in wealth, have slowed down the residential mobility likely to desegregate the city. In the former whites-only neighborhoods, for example, racial diversity diminishes as prices rise. Conversely, in black and Coloured townships, racial diversity remains very low, as residential mobility has done little to desegregate them. Racial diversity therefore arises in a price range where it is possible to access home ownership on credit with little or no down payment, i.e. between 700,000 and 1.2 million rand. [4] Racial diversity is therefore the highest in the metropolitan area in this window of change created by banking products. Two types of neighborhood are predominantly concerned: the old, whites-only areas of the old urban fabric, located along transport infrastructures; and the new neighborhoods on the northern and eastern outskirts of the city, also characterized by a dynamic rental market.

Prices have been adjusted for inflation according to the value of the rand in 2016.

Author: Julien Migozzi, 2020. Source: Deeds Office.

The unequal spatial distribution of prices and the unequal social distribution of credit create differentiated market regimes that structure the evolution of urban segregation. While professionals in the real-estate and banking industries, from France to India to the United States, have been increasingly quick in recent years to adopt digital technologies in the wake of PropTech and FinTech, the real-estate market in Cape Town highlights the fact that this renewal of market practices has first and foremost had the effect of reproducing long-term inherited inequalities.

Bibliography

- Breckenridge, K. 2014. Biometric State. The Global Politics of Identification and Surveillance in South Africa, 1850 to the Present, Cambridge: Cambridge University Press.

- Fourcade, M. and Healy, K. 2017. “Seeing Like a Market”, Socio-Economic Review, vol. 15, no. 1, pp. 9–29.

- James, D. 2014. Money from Nothing. Indebtedness and Aspiration in South Africa, Stanford: Stanford University Press.

- Migozzi, J. 2020. “Selecting Spaces, Classifying People: The Financialization of Housing in the South African City”, Housing Policy Debate, vol. 30, no. 4, pp. 640–660.

- Seekings, J. and Nattrass, N. 2005. Class, Race, and Inequality in South Africa, New Haven: Yale University Press.

- Shaw, J. 2020. “Platform Real Estate: Theory and Practice of New Urban Real Estate Markets”, Urban Geography, vol. 41, no. 8, pp. 1037–1064.

- Western, J. 1981. Outcast Cape Town, Berkeley: University of California Press.